Funding

Event Center Funding

The Auditorium District statute, as defined by the State Legislature, specifically prohibits the assessment of property taxes as part of the powers granted to the Board of Trustees for the Auditorium District. In addition, local option sales taxes are likewise prohibited by the State (in towns larger than 25,000 population). Therefore, the funding for the Event Center CANNOT become a local taxpayer issue.

Funding for the Event Center will be derived from two sources:

1. The Idaho Falls Auditorium District; and

2. Proceeds from operations (ticket sales, concessions sales, naming rights, advertising, souvenirs, etc.)

Likewise there will be two expenditure streams:

1. The mortgage or lease expenditure for the actual facility; and

2. The cost of operations (staffing, lights, heat, water, maintenance, etc.)

• The Auditorium District funds (fees collected at the hotels) will pay for the cost of constructing the facility.

• Proceeds from operations will be used to pay for the cost of operations.

This is an important distinction. By keeping these two expenditures separate, payment for the cost of constructing the facility will never be dependent upon the success of the operations. In fact, even if there were never a single event held in the Event Center, the cost of construction would still be paid for because of the Auditorium District. In turn, with no debt structure burden, operations have the maximum opportunity to succeed.

Debt Service on Construction

Based upon the financial models provided to us, while using today’s interest rates and terms, $1.5 million would pay for a loan of approximately $20 million. Since the construction costs are estimated to be approximately $28 million, the remaining balance of $8 million will have to be acquired through grants, investment by sports leagues, concessionaires, facility operators, ticket outlets and so on. All of which is very typical in these types of financial arrangements. In the end, the design of the facility may have to be adjusted to match the amount of money available. In no case will the amount of money borrowed exceed the payment that can be derived from the collection of the Auditorium District fees.

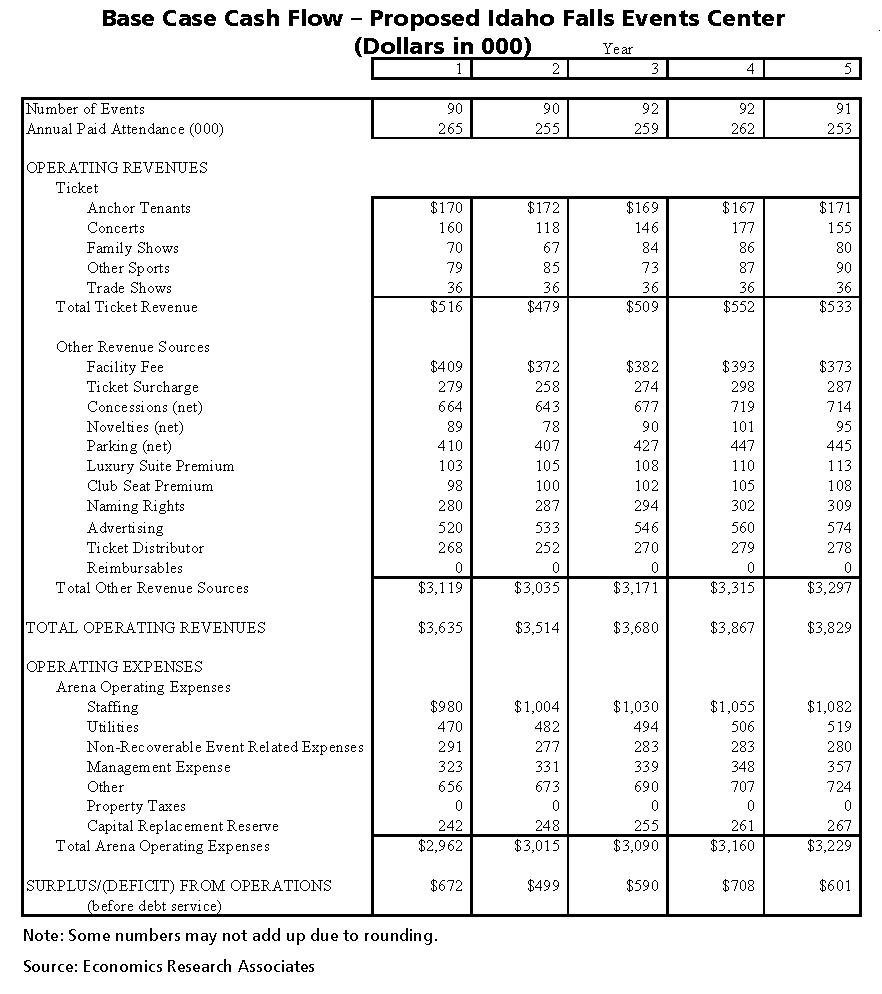

Operational Costs

Below is a financial model for the events center Base Case Cash Flow summaries for the proposed Event Center for the first five years of operation.